Mississippi PERS: An Overview

What’s going on?

The Mississippi Public Employees’ Retirement System (PERS) faces significant financial and structural challenges – and Mississippians deserve to know more about this complex issue. After all, changes to the system directly affect our citizens’ pocketbooks.

Last December, the PERS Board voted to increase taxpayer funding – referred to as the “employer contribution rate” – to shore up the struggling system. This action would have increased the taxpayer contribution rate by 5 percentage points (to 22.4% of payroll) at a whopping new cost of $345 million. This is on top of the $1.24 billion taxpayers already contribute to the system. The mechanism for that contribution is the employer contributions at the payroll level.

The PERS Board vote was not unanimous, with State Treasurer David McRae, State Revenue Commissioner Chris Graham, and retiree representative (and former State Insurance Commissioner) George Dale opposing the rate hike. Many legislators also balked at this proposal, with at least one bill filed to prohibit these increases from taking place.

On February 28, the PERS Board made another crucial vote: to delay implementation of the increased rate until July 1, 2024, kicking the issue down the road until next legislative session.

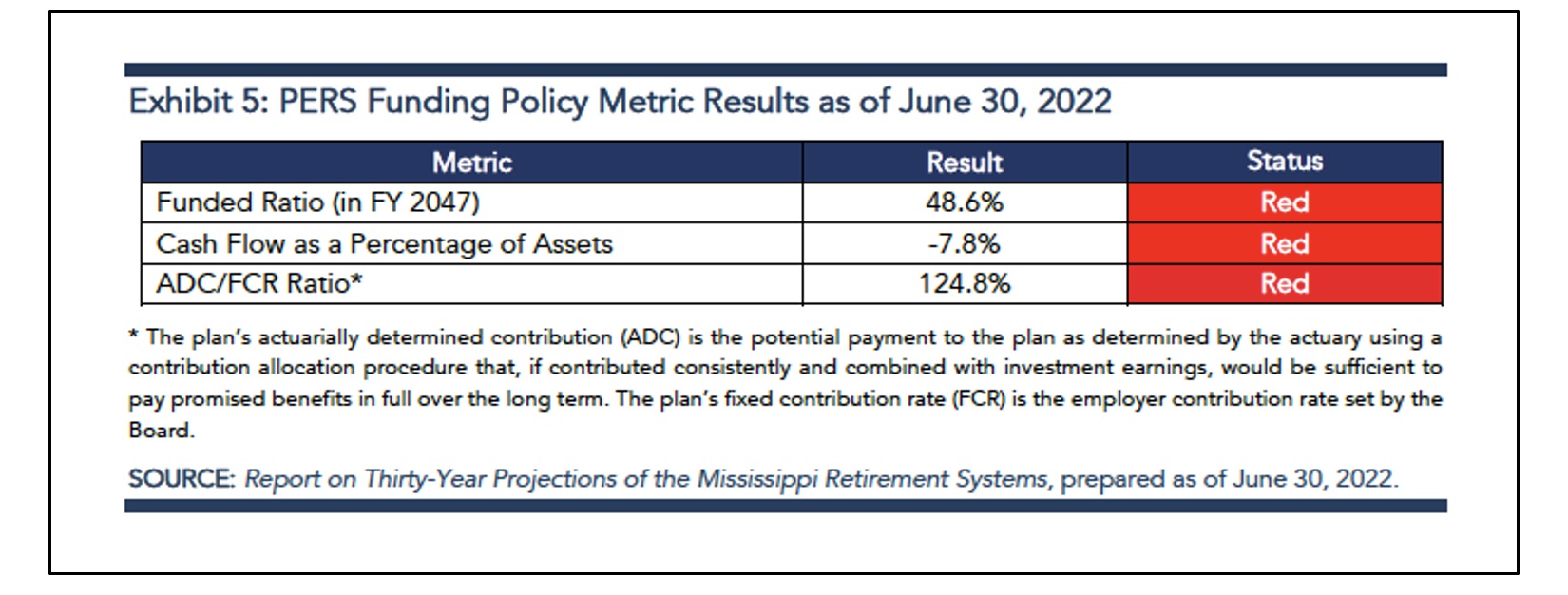

In the meantime, the legislative watchdog committee known as PEER (Performance Evaluation & Expenditure Review) just released new analysis of the system, finding that “all three of the plan’s funding policy metrics reached red signal-light status.”

The bottom line

PERS needs sensible changes to ensure its long-term viability. Policymakers owe it to retirees, state employees, and taxpayers to tackle one of the state’s largest unfunded liabilities.

A brief history of the plan

PERS is a governmental defined benefit retirement plan for a majority of employees of state agencies, counties, cities, colleges and universities, public school districts, and other such political subdivisions. It was created in 1952 by the Mississippi Legislature with broad support among lawmakers. For more historical information about the retirement system, visit the PERS history page. As of fiscal year 2022, PERS covered about 144,000 active members.

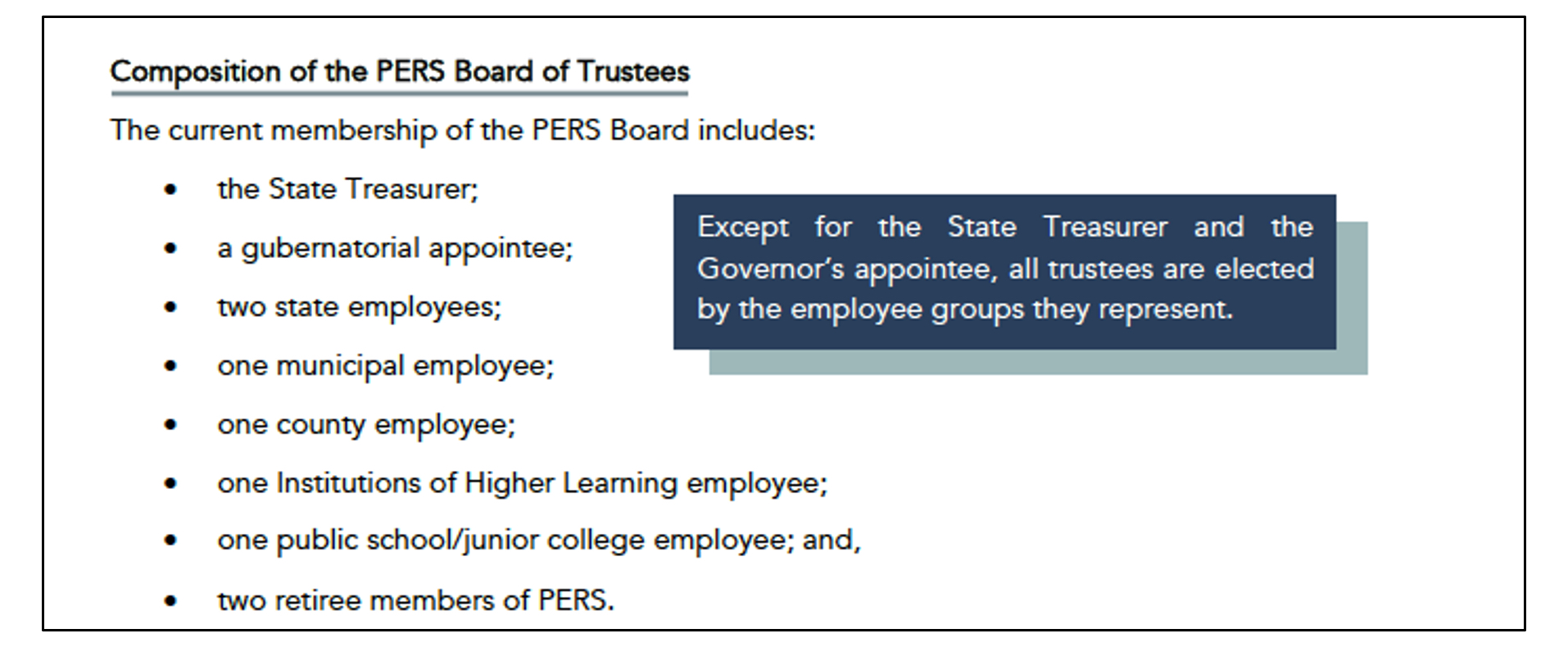

PERS is governed by a 10-member Board of Trustees, which includes the state treasurer, one gubernatorial appointee who must be a member of PERS, two state employees, two PERS retirees, one representative of public schools and community/junior colleges, one representative of the state’s institutions of higher learning, one representative of municipalities, and one representative of counties. Just two of the ten members represent non-employee groups, leaving taxpayers with little representation on the board.

The plan is funded through three primary avenues:

- contributions from members (public employees);

- contributions from employers (taxpayers); and

- investment earnings.

Retirement benefits vary based on an employee’s start date. Most employees in the system are “vested” (read: entitled to benefits) after four years and are eligible to retire after working 25 years and/or reaching the age of 60. The benefit formula calculation is generally two percent of “average compensation” times creditable service years (up to 25 or 30). (Average compensation is based on a member’s “high four,” meaning the four highest years of salary).

Notably, the PERS plan provides a cost-of-living adjustment, more commonly known as the “13th check,” to eligible retirees. The COLA is not tied to inflation or economic trends; it is a fixed rate of three percent and compounds after age 55 or 60, depending on retirement tier.

Sign up for BPF’s latest news here.